The New Global Chessboard

How EU, US, and China are Securing Critical Raw Materials for Industrial Survival

Introduction: The Silent Battle for the Elements

A silent, high-stakes battle is being waged across the globe. It is a conflict not for territory or ideology in the traditional sense, but for the fundamental elements that power our modern world. From the lithium in our smartphone batteries to the rare earth magnets in wind turbines, and from the gallium in advanced semiconductors to the titanium in fighter jets, a select group of minerals has become the bedrock of economic prosperity, technological leadership, and national security. The era of assuming cheap, abundant, and politically neutral supply chains for these materials is definitively over.

The divergent approaches of the world’s three largest economic blocs—the European Union, the United States, and China—to classifying and securing these “critical raw materials” reveal their unique industrial vulnerabilities, strategic ambitions, and geopolitical calculations. Each has developed its own “periodic table of risk,” a strategic roadmap that dictates industrial policy, trade relations, and international alliances. This article analyzes how each power is anticipating future shortages and actively reshaping global supply chains to ensure their industrial survival, using their distinct risk perspectives as a guide.

Chapter 1: The European Union – A Quest for Strategic Autonomy

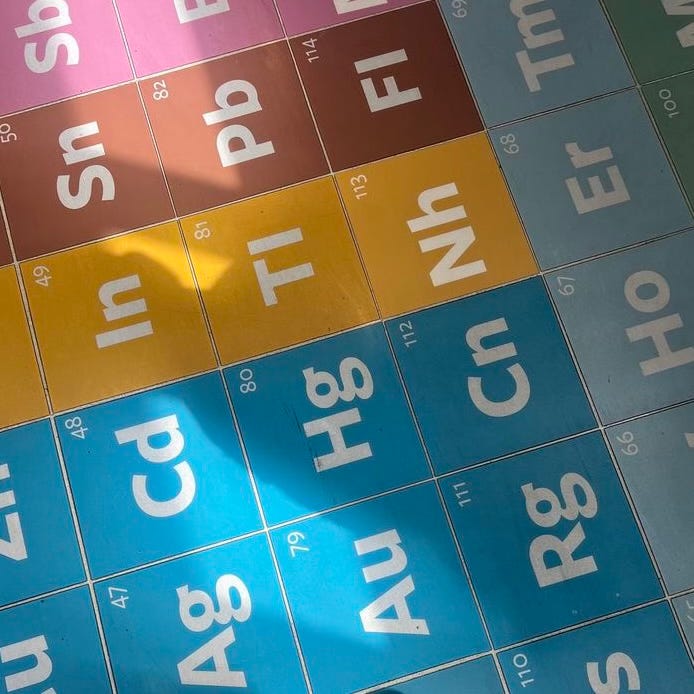

For decades, the European Union championed a model of deindustrialization and regulatory leadership, offshoring its heavy industries while focusing on high-value services and environmental standards. This strategy has now collided with a harsh reality: the EU is critically dependent on imports for the very materials needed to achieve its ambitious twin transitions—the Green Deal and the Digital Decade. The EU’s own analysis paints a stark picture of vulnerability, with its periodic table highlighting extreme supply risks for materials like heavy rare earths, magnesium, and graphite, nearly all of which are sourced from a single country: China .

Figure 1: The EU’s periodic table, color-coded by Supply Risk (SR). The prevalence of red and orange highlights extreme dependence on a few external suppliers for materials vital to its green and digital industries.

In response, Brussels has launched its most ambitious industrial policy in a generation: the Critical Raw Materials Act (CRMA). This legislation is the cornerstone of the EU’s quest for “strategic autonomy” and is built on three core pillars designed to fortify the bloc from within and diversify its external dependencies.

The EU’s Playbook: The Critical Raw Materials Act

The first pillar aims to fortify the home front by setting aggressive domestic capacity targets for 2030. The CRMA mandates that the Union should be able to produce 10% of its annual consumption in extraction, 40% in processing, and 25% in recycling . To achieve this, the act introduces the concept of “Strategic Projects,” which will benefit from streamlined and predictable permitting processes, aiming to overcome the notorious delays that have historically plagued mining and industrial projects in Europe.

The second pillar focuses on diversifying imports through Strategic Partnerships. A core tenet of the CRMA is the “65% Rule,” which stipulates that the Union should not be dependent on a single non-EU country for more than 65% of its supply of any strategic raw material by 2030. This is a direct response to dependencies like the 95% reliance on China for magnesium or the 100% reliance for heavy rare earths. To meet this goal, the EU is leveraging its “Global Gateway” investment program to fund infrastructure and build reliable supply chains with resource-rich countries, signing partnerships with nations like Canada, Chile, Australia, Kazakhstan, and Namibia.

Finally, the third pillar is dedicated to building a robust circular economy. Recognizing that the cheapest and most secure source of materials is waste, the CRMA places significant emphasis on “urban mining.” This involves creating a competitive market for secondary raw materials by promoting recycling, improving waste collection, and developing technologies to recover critical materials from discarded products like batteries, electronics, and magnets.

These strategies are forcing a paradigm shift in key European industries. The automotive sector, facing intense competition in the electric vehicle (EV) market, is now actively investing in battery gigafactories with integrated recycling capabilities. The renewable energy sector is exploring new wind turbine designs that use fewer rare earth magnets. For Europe, securing raw materials is no longer a matter of procurement; it is a matter of industrial survival.

Chapter 2: The United States – A National Security Imperative

Across the Atlantic, the United States frames the critical minerals issue primarily as a direct threat to its national security. The decades-long offshoring of manufacturing to Asia has created profound vulnerabilities in the defense industrial base and high-tech sectors. The US periodic table, based on import dependence, is a stark illustration of this risk, showing a startling 100% import reliance for 17 key minerals, including graphite, manganese, and rare earths—many of which are controlled by its chief geopolitical rival, China .

Figure 2: The US periodic table, color-coded by import reliance. The vast swaths of red underscore a near-total dependence on foreign nations for materials essential to defense, technology, and energy sectors.

Washington has responded with a whole-of-government legislative arsenal aimed at rapidly onshoring and “friend-shoring” critical supply chains. This represents the most significant shift in American industrial policy since the Cold War.

The US Playbook: A Legislative Arsenal

The Inflation Reduction Act (IRA) is a central weapon in this strategy. It provides powerful tax credits for consumers and manufacturers of EVs and batteries, but with a crucial string attached: the materials and components must be sourced from the US or its designated free-trade partners. The legislation explicitly excludes materials processed by “foreign entities of concern,” a clear directive aimed at decoupling the American EV supply chain from China.

Complementing the IRA, the CHIPS and Science Act allocates over $50 billion to revitalize the domestic semiconductor industry. This funding extends beyond chip fabrication to encompass the entire supply chain, including the materials essential for chip production like high-purity silicon, gallium, and germanium—all minerals where China holds a dominant market position.

To accelerate this industrial renaissance, the US government is intervening directly in the market. The Infrastructure Investment and Jobs Act allocates billions to co-fund the development of domestic mines, processing facilities, and battery recycling plants. Furthermore, the Department of Defense has repeatedly invoked the Defense Production Act (DPA) to provide direct grants and purchase commitments to companies building out domestic capacity for rare earth processing, lithium mining, and cobalt refining.

On the international front, the US is building a “buyers’ club” of allied nations. The Minerals Security Partnership (MSP) brings together Western powers and key resource-rich countries to jointly identify, de-risk, and finance strategic mining and processing projects outside of China. This initiative aims to create a parallel, secure supply chain for its members, effectively creating a market large enough to compete with China’s scale. This is further supported by the expansion of the National Defense Stockpile to buffer against acute supply shocks.

This aggressive, multi-pronged strategy is forcing a realignment of global investment flows. For the United States, the goal is clear: to build resilient, secure, and ideologically aligned supply chains for the foundational technologies of the 21st century, from defense systems to the clean energy grid.

Chapter 3: China – The Master of the Dual Strategy

China’s perspective on critical minerals is unique and far more complex than that of the EU or the US. It is simultaneously the world’s largest producer and processor of many critical minerals and, by a large margin, the world’s biggest consumer. Its strategic challenge is therefore twofold: how to leverage its current dominance for geopolitical gain while simultaneously securing the vast quantities of resources it lacks to feed its massive industrial apparatus.

Figure 3: China’s periodic table, based on strategic importance. It reveals a dual focus: leveraging its dominance in “advantage minerals” (marked with a star for export control) while prioritizing the acquisition of “scarce minerals” like lithium and nickel.

This has led to a sophisticated dual strategy that combines offensive market control with a defensive, long-term resource acquisition plan.

The Chinese Playbook: Geopolitical Leverage and Supply Security

First, China has demonstrated its willingness to weaponize its dominance in what it terms “advantage minerals.” Since 2023, Beijing has systematically imposed export controls on a growing list of materials where it holds a commanding market share. This includes gallium and germanium (essential for semiconductors), graphite (essential for EV batteries), and a range of rare earth elements . These actions are not random; they are carefully calibrated to create chokepoints in Western supply chains, often in direct response to US sanctions on China’s tech sector. The message is clear: if you restrict our access to technology, we will restrict your access to the materials needed to build it.

Second, while flexing its muscles as a producer, China is aggressively addressing its own significant vulnerabilities in “scarce minerals.” Its top strategic priorities include lithium, nickel, and cobalt—the holy trinity of battery manufacturing—where it has very little domestic production. To secure these, China has pursued a multi-decade “going out” strategy. This involves its state-owned enterprises making massive investments to acquire majority stakes in mines across Africa (cobalt in the Democratic Republic of Congo) and Latin America (lithium in Chile and Argentina). Through its Belt and Road Initiative (BRI), China has also financed ports, railways, and power plants across the developing world, often in exchange for long-term offtake agreements that lock in decades of mineral supply.

This dual strategy has been remarkably effective. It has allowed China to build a commanding, and in some cases monopolistic, position across the entire value chain for key future industries. In the EV sector, for example, China not only hosts the world’s largest vehicle market but also controls over 75% of global battery cell production, 85% of anode material production, and 90% of battery-grade lithium processing. This deep integration makes global supply chains for the green transition heavily dependent on Chinese industrial policy and geopolitical goodwill.

Conclusion: A New Era of Geopolitical Competition

The three divergent periodic tables of risk are not mere academic exercises; they are strategic roadmaps that are actively dictating industrial policy, shaping trade relations, and redrawing the map of geopolitical alliances. The world is rapidly fragmenting into competing supply chain blocs, with the EU, US, and China each striving to build a resilient and ideologically aligned ecosystem.

This fragmentation is driven by a great paradox: the global push for a “green” energy transition is intensifying geopolitical competition for a handful of “dirty,” difficult-to-mine, and geographically concentrated minerals. The path to decarbonization, it turns out, runs directly through some of the world’s most challenging geopolitical terrain, from the lithium brines of the Andes to the cobalt mines of the Congo and the rare earth processing plants in China.

For global industries, the implications are profound. Navigating this new landscape is no longer a simple procurement issue to be managed by the purchasing department; it is a core strategic challenge that demands the attention of the C-suite and the board. The era of assuming stable, efficient, and politically neutral globalized supply chains is over. In its place is a new reality where resilience, traceability, and geopolitical risk assessment are paramount for survival. The companies that thrive in the coming decade will be those that understand this new global chessboard and move decisively to secure their position on it.